ADDRESS

Khurrampur, Farrukh Nagar, Haily Mandi Road, Gurgaon, Delhi (NCR)

Financial Derivatives

About Financial Derivatives

Financial derivatives are financial instruments the price of which is determined by the value of another asset. Such an asset, ie the underlying asset, can in principle be any other product, such as a foreign currency, an interest rate, a share, an index or a commodity.

Financial derivatives are financial instruments that are linked to a specific financial instrument or indicator or commodity, and through which specific financial risks can be traded in financial markets in their own right. Transactions in financial derivatives should be treated as separate transactions rather than as integral parts of the value of underlying transactions to which they may be linked. The value of a financial derivative derives from the price of an underlying item, such as an asset or index. Unlike debt instruments, no principal amount is advanced to be repaid and no investment income accrues. Financial derivatives are used for a number of purposes including risk management, hedging, arbitrage between markets, and speculation.

Financial derivatives are contracts that derive their value from the performance of an underlying asset, index, or interest rate. The underlying asset can be a stock, bond, commodity, currency, or even another derivative. Derivatives are used for a variety of purposes, including hedging, speculation, and arbitrage.

Financial derivatives enable parties to trade specific financial risks (such as interest rate risk, currency, equity and commodity price risk, and credit risk, etc.) to other entities who are more willing, or better suited, to take or manage these risks—typically, but not always, without trading in a primary asset or commodity. The risk embodied in a derivatives contract can be traded either by trading the contract itself, such as with options, or by creating a new contract which embodies risk characteristics that match, in a countervailing manner, those of the existing contract owned. This latter is termed offsetability, and occurs in forward markets. Offsetability means that it will often be possible to eliminate the risk associated with the derivative by creating a new, but "reverse", contract that has characteristics that countervail the risk of the first derivative. Buying the new derivative is the functional equivalent of selling the first derivative, as the result is the elimination of risk. The ability to replace the risk on the market is therefore considered the equivalent of tradability in demonstrating value. The outlay that would be required to replace the existing derivative contract represents its value—actual offsetting is not required to demonstrate value.

Financial derivatives contracts are usually settled by net payments of cash. This often occurs before maturity for exchange traded contracts such as commodity futures. Cash settlement is a logical consequence of the use of financial derivatives to trade risk independently of ownership of an underlying item. However, some financial derivative contracts, particularly involving foreign currency, are associated with transactions in the underlying item.

Date : 07 Oct, 2023

Financial Derivatives

WEB DESIGNING

10 Nov, 2019

view gallery

PHP

AUTOCAD 2020

DIGITAL MARKETING

OFFICE 365

10 Nov, 2019

view gallery

MEAN STACK

10 Nov, 2019

view gallery

SOLID WORKS 2016

10 Nov, 2019![]()

REVIT STRUCTURE

JAVA TRAINNG

10 Nov, 2019

view gallery

HTML TRAINING

WEB DEVELOPMENT

EMBEDDED SYSTEM

10 Nov, 2019

view gallery

Embedded Hardware

C Language

CCNA

Tax Auditor

10 Nov, 2019

view gallery

Entrepreneurship Development Program

Finance Manager

Database Administrator

System Administrator

10 Nov, 2019

view gallery

Information System Manager

Computer Science Technology

Computer and Information Research Scientist

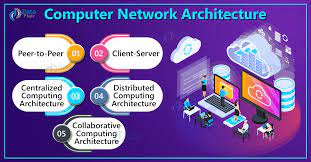

Computer Network Architects

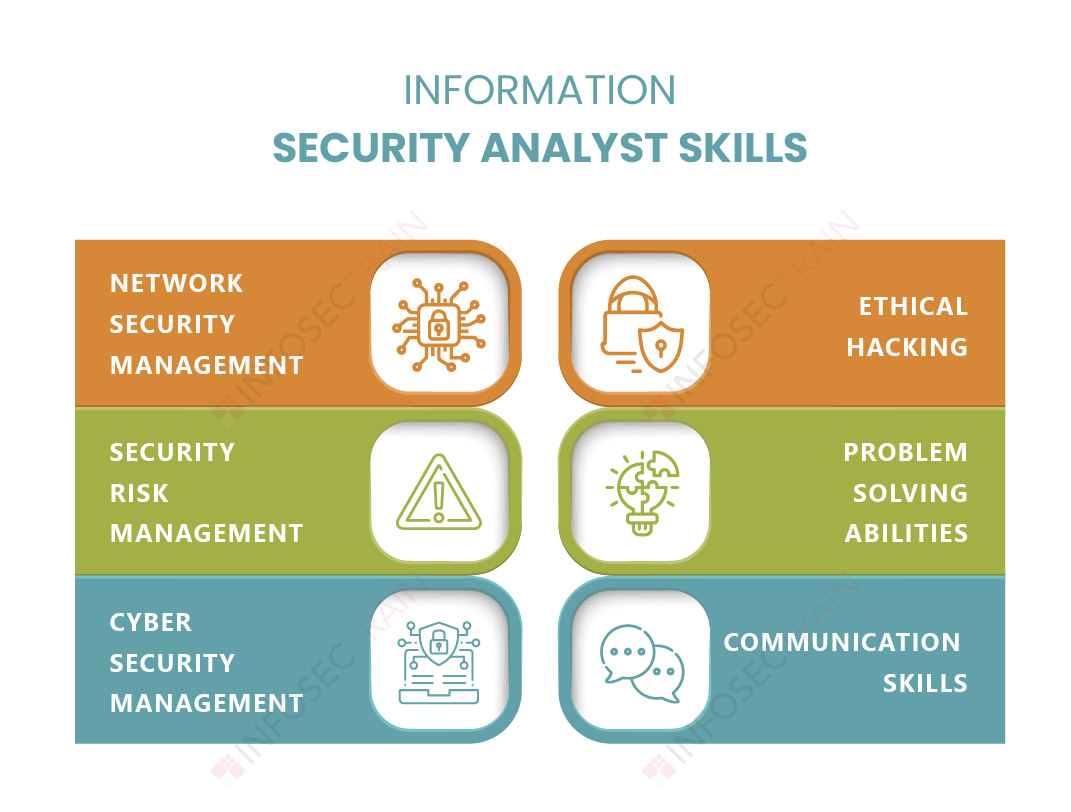

Information Security Analyst

10 Nov, 2019

view gallery

Database Administrators and Architects

Data Mining

Deep Learning

Computer Vision

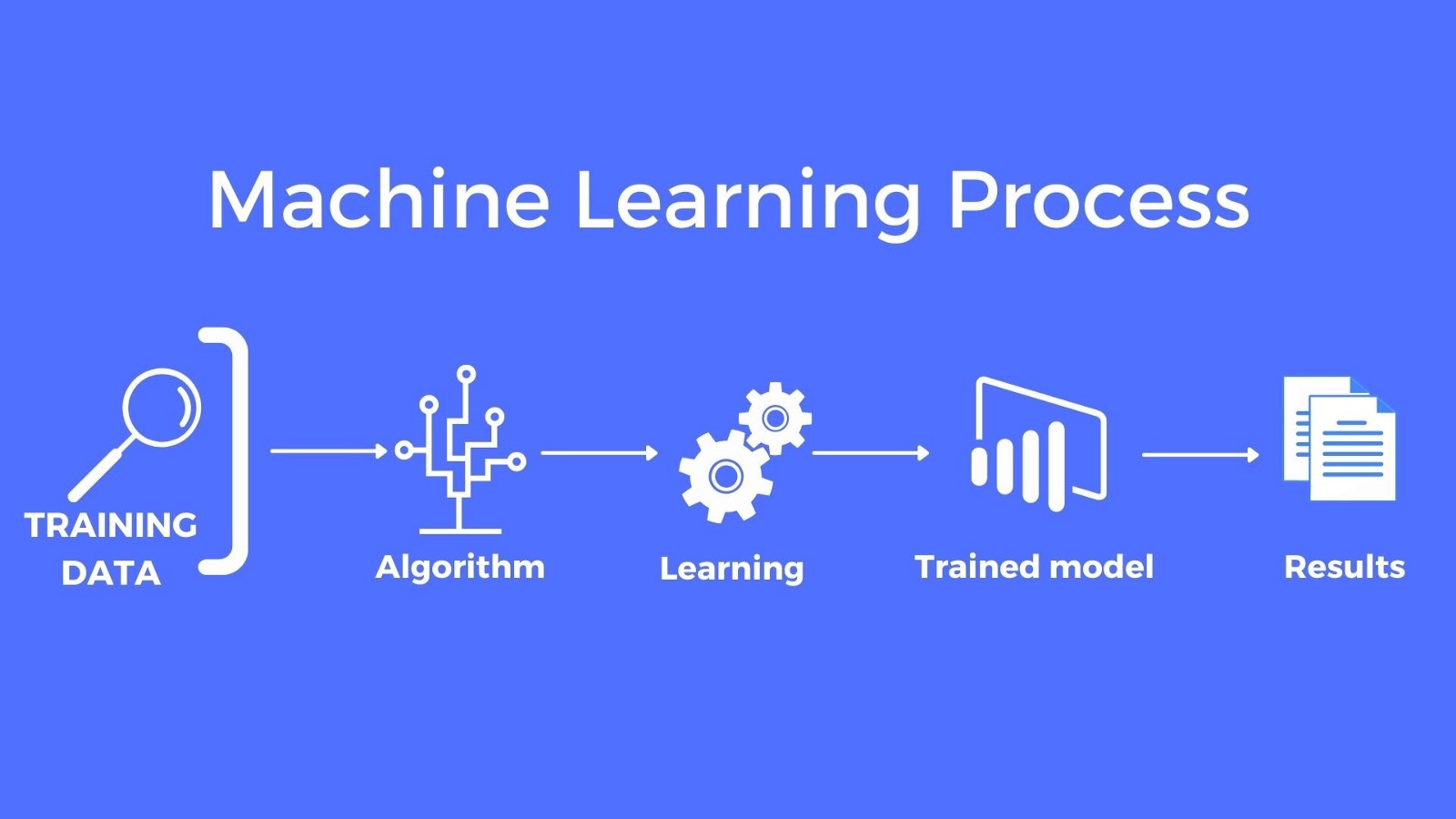

Machine Learning

Big Data Analytics

Neural Networks

Statistics Mathematics

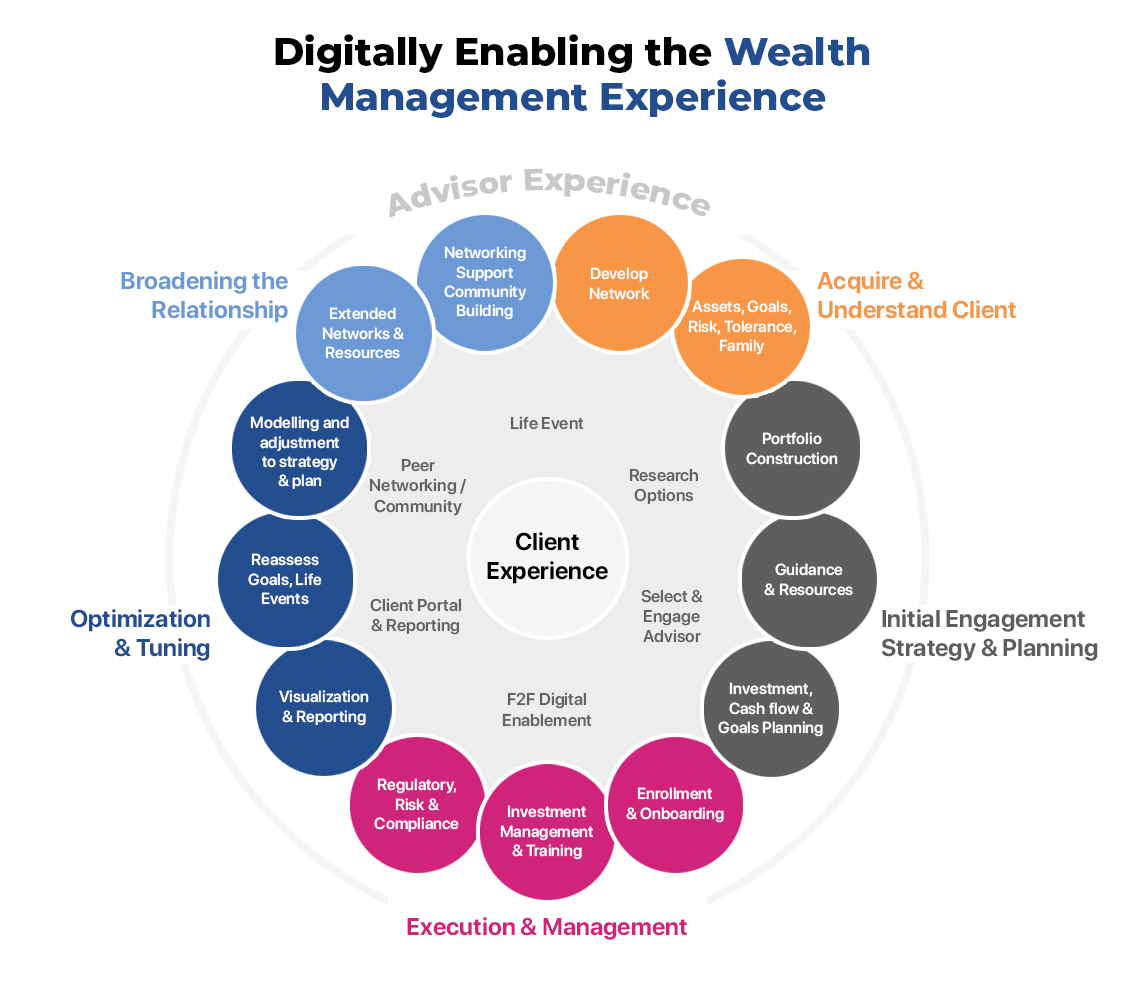

Wealth Management and Financial Planning

10 Nov, 2019

view gallery

SAP ERP

Personality Grooming

Recruitment Process

10 Nov, 2019

view gallery

Data Visualization

Service Engineer

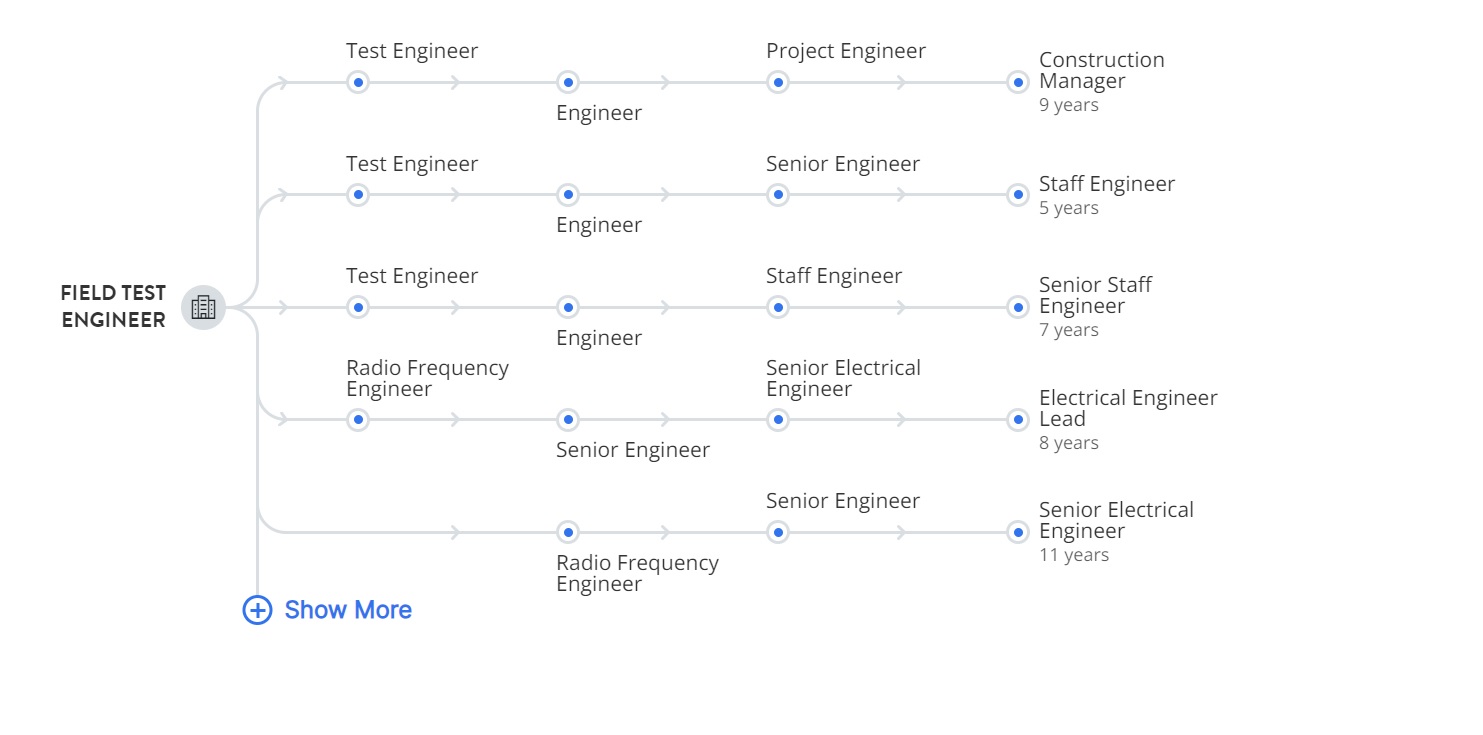

Field Test Engineer

10 Nov, 2019

view gallery

Technical Director

Software Developer

Programmer Analyst

10 Nov, 2019

view gallery